China's chokehold on rare earths & its impact on India (and others)

How did the rare earth magnets issue arise? How does this impact India? What steps can India take in the short to long term to address this challenge?

How a bilateral trade war became a global challenge:

In May 2025, the White House announced a “historic trade win” for the United Stated after it reached an agreement with China to “reduce China’s tariffs and eliminate retaliation, retain a U.S. baseline tariff on China, and set a path for future discussions to open market access for American exports.”

This truce followed an escalating trade war between the two countries after the United States raised tariffs on Chinese imports from 20.8% on January 1, 2025 to 30.8% on February 4, and then from 42.1% on April 3 to an eye-watering 134.7% on April 10 [see figure 1].

The two sides pulled back from the brink and following a meeting in Geneva in May, the “effective tariff rate on Chinese imports was reduced to 30%, while the Chinese tariff rate on American goods was reduced to 10%.”

This understanding didn’t last long with each party accusing the other of “violating” the trade truce. According to U.S. Trade Representative Ambassador Greer, the Chinese responded to U.S.’s tariffs with a slew of measures including restrictions on the “exports of rare earth magnets, a critical component in cars, aircraft and semiconductors.” The Ambassador stated,

“They removed the tariff like we did but some of the countermeasures they’ve slowed on… The United States did exactly what it was supposed to do and the Chinese are slow-rolling their compliance which is completely unacceptable and has to be addressed.”

On the other side, China accused the United States of introducing a “series of discriminatory and restrictive measures” which included “warnings against the use of Huawei chips globally, a halt to sales of chip design software to Chinese companies, and the cancellation of visas for Chinese students.”

One of the key factors that led to the unravelling of the understanding reached in Geneva appears to be the export restrictions on rare earths that China instituted in early April. Per this New York Times report from April,

“Shipments of the magnets, essential for assembling everything from cars and drones to robots and missiles, have been halted at many Chinese ports while the Chinese government drafts a new regulatory system. Once in place, the new system could permanently prevent supplies from reaching certain companies, including American military contractors. The official crackdown is part of China’s retaliation for President Trump’s sharp increase in tariffs that started on April 2… On April 4, the Chinese government ordered restrictions on the export of six heavy rare earth metals, which are refined entirely in China, as well as rare earth magnets, 90 percent of which are produced in China. The metals, and special magnets made with them, can now be shipped out of China only with special export licenses.”

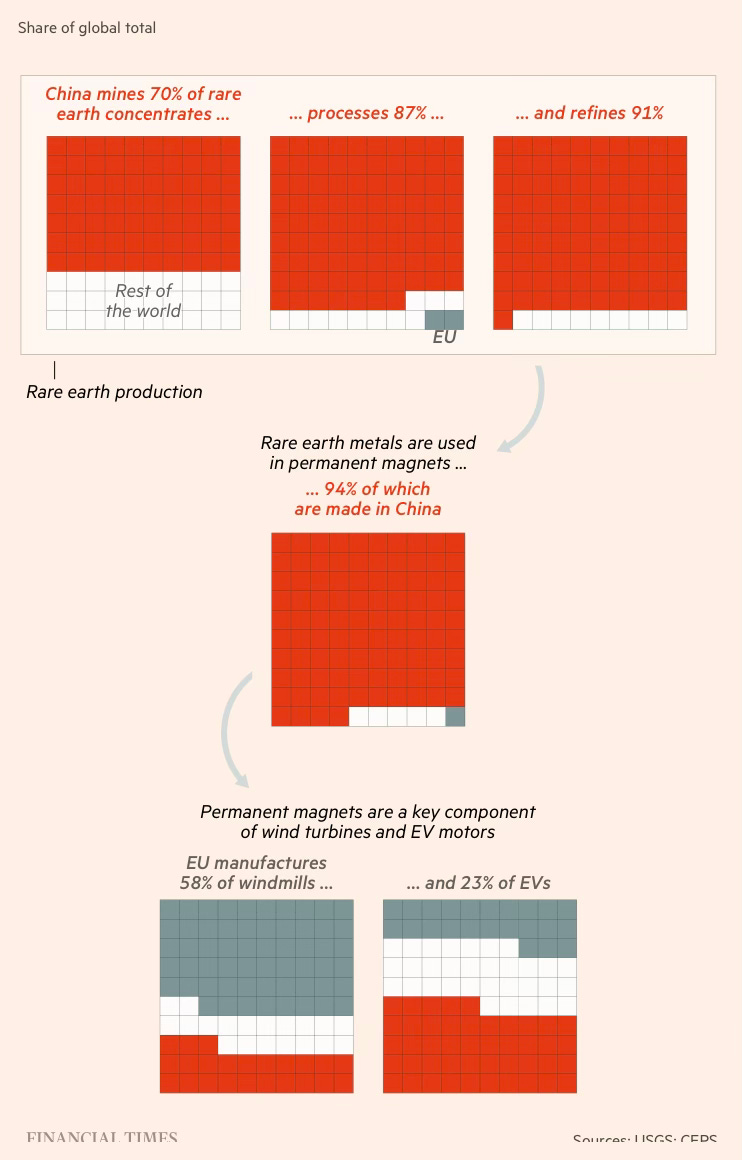

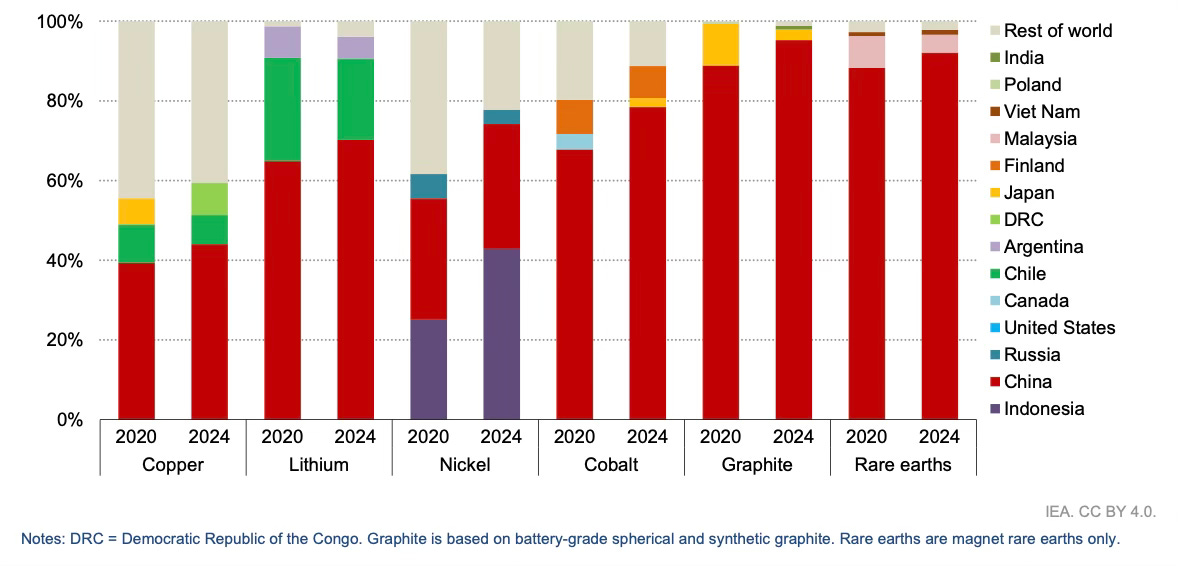

CSIS’ Gracelin Baskaran points out that the Chinese restrictions apply to “seven medium and heavy rare earths: samarium, gadolinium, terbium, dysprosium, lutetium, scandium, and yttrium” and that the United States is “particularly vulnerable for these supply chains” as, till 2023 “China accounted for 99 percent of global heavy REEs [rare earth elements] processing, with only minimal output from a refinery in Vietnam.” The Vietnamese site has been shut for the last year “effectively giving China a monopoly over supply” [see figure 2 & 3]. Per reports, shipments of rare earth magnets to the United States dropped by a stunning 60% from March to April.

A Precarious Truce:

This brings us to the current moment. On June 11, United States and China restored their ‘trade war truce’ following intense negotiations in London. The Wall Street Journal highlighted that it was,

“China’s chokehold on rare-earth exports that helped drive the parties to reconvene for the London talks, prompting the Trump administration to put U.S. export controls—a key hurdle for China’s industrial and technological ambitions—on the table for the London negotiations.”

According to a Guardian report on the matter,

“US and Chinese officials agreed on a framework to get their trade truce back on track and remove China’s export restrictions on the rare earth imports essential to US industries including automotive, electronics and defence, while offering little resolution to wider trade differences.”

The issue of access to rare earths appears to have settled but the situation remains highly precarious. The Chinese have placed a “six-month limit on rare-earth export licenses for U.S. automakers and manufacturers” which gives Beijing “leverage if trade tensions flare up again while adding to uncertainty for American industry.” The Wall Street Journal spoke to people who consult with Chinese officials who noted that,

“Beijing wants to retain its chokehold on the critical minerals to give it valuable ammunition for future negotiations.”

India (and the world) feel the heat:

China’s dominance in this sector isn’t a concern just for the United States [see figure 4]. The European Union’s Trade Commissioner said that this issue was a “priority” in a meeting with the Chinese commerce minister, telling reporters

“I informed my Chinese counterpart about the alarming situation in the European car industry, but I would say industry as such because clearly rare earths and permanent magnets are absolutely essential for industrial production.”

The secretary general of the European Association of Automotive Suppliers (CLEPA) said “China’s export restrictions are already shutting down production in Europe’s supplier sector.” The head of Germany’s auto lobby told Reuters that “production delays and even production outages can no longer be ruled out” if the situation doesn’t alter. The impact is being felt on the battlefield in Ukraine with the curb of magnets affecting the “delivery of drones and drone parts to Ukraine.” An industry executive at the Australian Strategic Materials Ltd. put the challenge more starkly, noting that China’s moves have “created an urgency… The phones are running hot, and they’re not just running hot from the US. Everyone is impacted by it.”

The Indian side has sounded the alarm as well. The Ministry of External Affairs’ spokesperson stated,

“The Chinese ministry of commerce and general administration of commerce, in early April, announced their decision to implement export controls on certain rare-earth related items… We remain in touch with the Chinese side, in Beijing as well as in Delhi, to bring predictability in supply chain for trade consistent with international practices.”

China’s rare earth restrictions were raised in a discussion between the Indian Foreign Secretary and the Chinese Vice Foreign Minister this past week. How precarious is this situation for India? According to this Bloomberg report,

“Indian automakers are facing conditions tougher than others in importing rare earth magnets from China, according to people familiar with the matter, risking a crippling shortage that may disrupt production within weeks.”

There also appears to be some inconsistency in how the Chinese government is imposing its restrictions. This is on top of an already onerous process that importers have to navigate.1 Alisha Sachdev, Sudhi Ranjan Sen, and Shruti Srivastava report -

“Beijing has turned down at least two applications for India-bound shipments, industry and government officials in New Delhi said, asking not to be identified because the discussions are private. A requested shipment to the Indian unit of a global firm was rejected by the Chinese government, while its German and US subsidiaries were allowed to import magnets, the people said on the condition of anonymity… At least 30 import applications have been endorsed by the Indian government but none of the companies have been approved nor have any shipments arrived, the people said. At least 11 applications from companies in the other parts of the world have passed muster.”

The Society of Indian Automobile Manufacturers (SIAM) made a presentation to Indian government officials on May 28 seeking “urgent talks between China and India to fast-track pending approvals and ease the onerous process.”

The export restrictions will sharply impact India’s growing electric vehicle industry in particular. Maruti Suzuki India, one of the top automobile manufacturers in the country has reportedly adjusted “production schedules for its forthcoming e-VITARA model due to rare earth magnet shortages” and is targeting the production of 8,000 units by September - down from an initial target of more than 26,000 units in the same timespan.

An executive at Bajaj Auto, India’s largest electric two-wheeler maker, stated the following on a conference call on May 29,

“The rare earth situation is a very difficult one… Supplies and stocks are getting depleted as we speak, and if there’s no relief in shipments, production will be seriously impaired in July. That’s currently the case for the entire auto industry.”

The direness of the situation for the Indian automotive sector can be gleaned from the fact that a “contingent of automotive industry delegates is preparing to visit China to facilitate rare earth magnet imports for Indian companies”.2 According to a report on this,

“Around 40-50 executives, representing both auto OEMs and component firms, have received visas and are now awaiting a go-ahead from China’s Ministry of Commerce for a meeting,” an industry source told PTI. A second source indicated that no authorisations have been granted thus far.”

This delegation visit is being facilitated by the Indian Embassy in Beijing which has also “reached out to China’s Commerce Ministry” for the “quick disposal of applications and transparency in the process.” At a meeting in the Indian Prime Minister’s Office to discuss “options for breaking this impasse” government officials “told the industry representatives to start working on alternative supply chains for rare earth minerals and develop indigenous refining capacity to pare reliance on China.” The Indian government has also advised companies to “explore ferrite magnets or magnet-free designs - options that come with trade-offs in cost and performance.”

The challenge with these ad-hoc solutions is that none of these measures ease the “immediate threat of disruption for Indian automakers.” Due to this, firms in India (and across the world) are forced to do what they can -

“Indian automakers have begun weighing expensive workarounds: importing motors or sub-assemblies, shifting focus to fossil-fuel fed vehicles or prioritizing exports over domestic EVs.”

The head of a German magnet maker told the Financial Times how major European carmakers have “asked for additional supplies to avoid a shutdown of production lines” further stating,

“Everybody started calling and said ‘can you give us 2,000 magnets because our line is going to stand still. The price is not an issue - let’s talk about what you can do, when can we have it, and how can you do it.’ It’s just unbelievable.”

India has gone to the extent of suspending a 13-year-old agreement on rare earth exports to Japan in order to “safeguard supplies for domestic needs” with India’s Commerce Minister Piyush Goyal asking state-run miner IREL (formerly Indian Rare Earths Ltd.) to “stop its exports of rare earths, mainly neodymium, a key material used in magnets for electric vehicle motors”.3 The Reuters report also goes on to note that India “may not immediately be able to stop supplies to Japan because they fall under a bilateral government agreement” with IREL aiming for this to be “amicably decided and negotiated because Japan is a friendly nation.”

Where does India go from here?

China’s export restrictions are here to stay. The Wall Street Journal highlighted the six-month limit that China placed on rare-earth export licenses for U.S. automakers and manufacturers. Critically, China is “unlikely to allow companies to build up inventories, especially in the defense industry.”

The head of research at Gavekal noted,

“They [China] might well be restarting enough of the export licenses so that the commercial buyers can get what they need… But they are not going to issue enough licenses so that people can stockpile. They are not going to give up their leverage.”

Given this reality, in the short to medium term, Indian firms will be forced to find workarounds and where possible, procure the requisite materiel at higher rates. The upcoming meetings between Indian and Chinese delegations to facilitate imports “could help the Narendra Modi government determine what could be China’s ask in return for easing the supplies of rare earth magnets.” Industry executives realise this limitation with one executive stating,

“The short-term solution has to be to get Chinese authorities to clear things… A radical shift in supply chain is not possible in the short term.”

Over a longer time horizon, the government can take a number of steps to ensure that it is able to establish reliable supplies of essential critical minerals.

Develop local extraction and processing capabilities: According to the International Energy Agency, India “possesses major untapped resource potential.” India houses the world’s fifth-largest rare earth reserves, at 6.9 million metric tons. In 2023, China processed over 200,000 tons of rare earths, compared to IREL’s 10,000 tons. According to Reuters, India “lacks wide-scale technology and infrastructure to mine rare earths, and the development of any commercially viable domestic supply chain is years away.” The government is reportedly taking steps to correct this. The government is drafting a scheme, under the aegis of the Ministry of Heavy Industries, to partially fund “the difference between the final price of the made-in-India magnet and the cost of the Chinese imports” and the government is in talks “with companies to establish long term stockpiles of rare earth magnets by offering fiscal incentives for domestic production.” The government needs to ensure that a realistic timeline is set for these ideas and schemes to translate into tangible action.

Work with like-minded partners to establish reliable supply chains: The impact of China’s export restrictions are reverberating globally. India has a strong relationship with many of the states that have been impacted, and could work with, to develop reliable supply chains. These include Australia, which has the “most advanced capabilities for the mining industry outside of China,” Japan, with its “advanced technical expertise,” the EU, and the United States. There are also extant platforms like the ‘Minerals Security Partnership’ which offers “an opportunity to move beyond symbolic agreements and build a market with sufficient scale to effectively challenge China’s dominance, using coordinated tariffs, quotas, and incentives.”

Establish a minerals research and development organisation: A June 2023 report on ‘Critical Minerals for India’ recommended establishing a ‘Centre of Excellence for Critical Minerals’ (CECM) that will “focus on identifying more efficient ways for discovering next generation critical mineral deposits through geographical knowledge, data analytics and modelling, and machine learning capability” and support the “building up of new research and analytical infrastructure to support India’s critical mineral demand.” This recommendation was reiterated in a press release on the ‘National Critical Mineral Mission’ in April 2025 but no such institution has been set up. The government can work with Australia’s ‘Commonwealth Scientific and Industrial Research Organisation’ (CSIRO)4 which is one of the world’s largest minerals research and development organisation to to build a first-rate institution domestically.

Institute financing and frameworks for critical minerals recycling: According to experts, the “promotion of recycling and the use of recycled materials for manufacturing inputs” reduce requirements from mines and also have sustainability benefits. E-waste recycling is a “promising avenue” that can “help recover critical minerals domestically” but current recycling levels are “abysmal” with India recycling around 22% of the 62 million tons of e-waste it generates annually. Recent reports note that an incentive scheme for recycling of critical minerals, including copper, lithium, nickel, cobalt, and rare earth elements, are currently in the final stage with plans to “capex subsidy to eligible recyclers.” The Union budget has also allocated INR 1500 crore for recycling critical minerals under the ‘National Critical Mineral Mission.’

Address China’s market-distorting practices: In an important piece, CSIS’ Gracelin Baskaran pointed out that a major challenge to “achieving mineral security is China’s manipulation of global markets, whereby Chinese companies flood the market with excess supply, driving prices down to levels that force mining operations in countries like the United States and Australia to shut down.” Projects outside China “need to promise higher investment returns to attract financing, whereas large Chinese state-owned companies can sustain operations at much lower-or even negative-profit margins.” If India, and other like-minded partners, are taking steps to ensure that there are reliable critical minerals supply chains, addressing China’s market-distorting practices is essential. This will be effective only if nations work together to challenge Chinese practices.5

Conclusion:

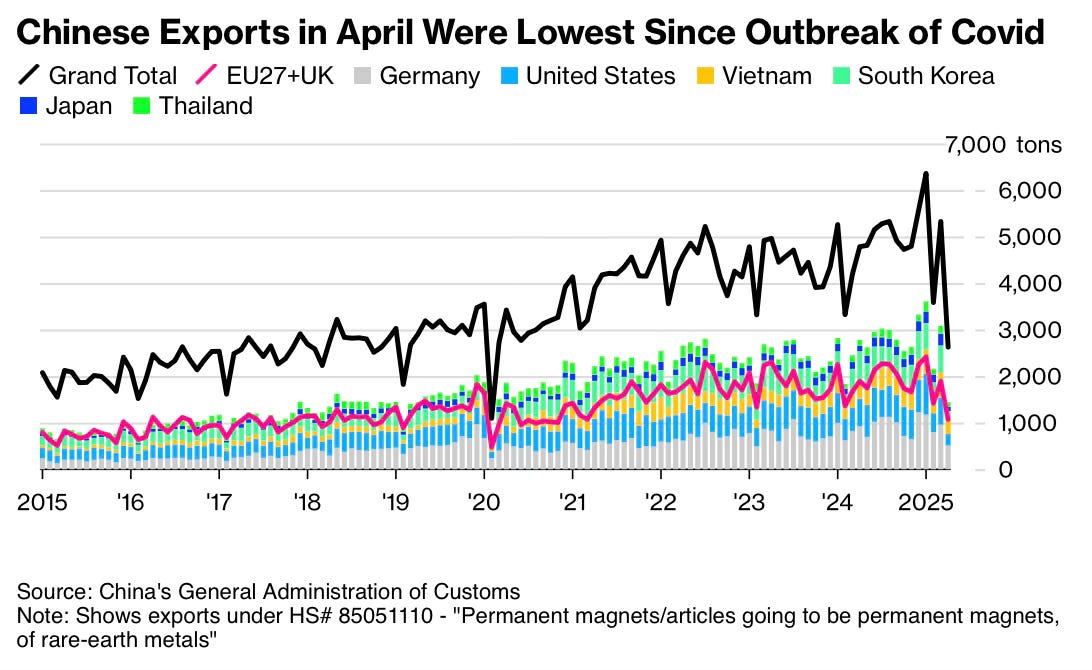

A Bloomberg headline on the matter sums up the current moment well [see figure 5].

With inventories of rare earth magnets expected to run dry within a month’s time, China’s rare earths exports control present a stark challenge to India. In 2024-25, India imported rare earth magnets worth around $200 million. While the trade value is “relatively modest,” the strategic reliance on China for these products has an outsized impact on India’s industries.

The hope is that this episode ignites a broader conversation within the Indian government and across industry on the consequences of excessive reliance on China for critical materials. This does appear to be the case with the Central Electricity Authority (CEA) recently proposing incentives “to domestic manufacturers producing critical components required in the power sector such as magnets and voltage transformers in a bid to reduce reliance on China.”

The problem is that we have seen this movie before. During the COVID-19 pandemic, India’s reliance on China for active pharmaceutical ingredients (APIs) that “adversely impacted the production of hydroxychloroquine” was seen as a “wake-up call.” Despite government efforts, imports from China continue to grow. In 2020, there were reports that India would curb Chinese power equipment imports. Five years later, the CEA is attempting to spur domestic manufacturers to produce “critical components required in the power sector.” Similar stories can be shared about India’s reliance on China for drones and batteries.

India’s Commerce Minister recently said that India is “actively building alternative supply chains while positioning itself as a trusted partner for international businesses seeking to reduce their dependence on Chinese suppliers” in reference to Chinese restrictions. He also described China’s rare earth export restrictions as a global “wake-up call.” One can only hope that this alarm translates into action.

Further reading:

I have highlighted select works that readers might refer to for a better understanding of the issues at play (arranged in chronological order).

Amid China's Tantrums, India’s Hardware Warriors Are Battling to Build Rare Earth-Free EV Motors, Rakshit Kumar, Outlook [June 16, 2025]

India moves to conserve its rare earths, seeks halt to Japan exports, sources say, Neha Arora and Aditi Shah, Reuters [June 15, 2025]

China-backed militia secures control of new rare earth mines in Myanmar, Naw Betty Han, Shoon Naing, Devjyot Ghoshal, Eleanor Whalley and Napat Wesshasartar, Reuters [June 12, 2025]

China’s Lock on Rare Earths Dictated Path Toward Trade Truce, Jon Emont and Gavin Bade, The Wall Street Journal [June 11, 2025]

New China Trade ‘Deal’ Takes U.S. Back to Where It Started, Ana Swanson, The New York Times [June 11, 2025]

An Emergency Trade Discussion With Joey Politano, Paul Krugman, Substack [May 31, 2025]

Trump's Retreat Still Leaves Tariffs at 90-Year Highs, Joseph Politano, Apricitas Economics [May 19, 2025]

Critical minerals: India must step up its strategies, Saloni Sachdeva Michael, Institute for Energy Economics and Financial Analysis [April 24, 2025]

Critical minerals: Goals and gaps, Rakshith Shetty, Deccan Herald [February 5, 2025]

Critical Minerals and Great Power Competition, Jiayi Zhou and Andre Manberger, SIPRI [October 2024]

Critical Materials Are In High Demand. What is DOD Doing to Secure the Supply Chain and Stockpile These Resources? U.S. Government Accountability Office [September 12, 2024]

Projecting Critical Mineral Needs for India’s Clean Energy Transition: How Much of Which Minerals Are Needed for the Transition? Rajesh Chadha and Ganesh Sivamani, Centre for Social and Economic Progress [June 2024]

How Japan solved its rare earth minerals dependency issue, Tatsuya Terazawa, World Economic Forum [October 13, 2023]

The U.S. Government Should Stockpile More Critical Minerals, Gregory Wischer and Jack Little, War on the Rocks [September 27, 2023]

Revisiting the China–Japan Rare Earths dispute of 2010, Simon Everett and Johannes Fritz, VoxEU [July 19, 2023]

Critical Minerals for India, Report of the Committee on Identification of Critical Minerals, Ministry of Mines, Government of India [June 2023]

Magnet manufacturing process, Magnosphere [accessed June 14, 2025]

A Bloomberg report by Alisha Sachdev, Sudhi Ranjan Sen, and Shruti Srivastava underscores this fact - “Indian firms are navigating a complex certification maze involving more than half a dozen steps: securing notarized and apostilled documents, getting them endorsed by the Chinese embassy and sending it to exporters in China.” China also “requires importers to submit an application detailing the end-use of rare earth magnets, with assurances that the materials won’t be used in military applications or routed to the US.” This process needs to be “initiated by the importer, then endorsed by Chinese authorities before being submitted for final clearance.” In mid-May, the chief executive of Mahindra & Mahindra’s auto unit said that the process for obtaining end-use certification “is not clear at the moment.” A Financial Times article reported on worries among European companies who were “not sure how to prove” that their shipments wouldn’t be re-exported to the United States in breach of the licensing conditions. While some licences are being denied by the Chinese on procedural grounds, other firms are being asked to disclose sensitive information. A Financial Times report on the matter quoted a senior trade body executive stating that “there are only a headful of [Chinese] officials reviewing thousands of applications.”

As stated above, this is a global problem. It’s not just Indian delegations that are headed to China. According to Reuters, “A business delegation from Japan will visit Beijing in early June to meet the Ministry of Commerce over the curbs and European diplomats from countries with big auto industries have also sought “emergency” meetings with Chinese officials in recent weeks.”

According to Reuters, “Under a 2012 government agreement, IREL supplies rare earths to Toyotsu Rare Earths India, a unit of Japanese trading house Toyota Tsusho which processes them for export to Japan where they are used to make magnets. In 2024, Toyotsu shipped more than 1,000 metric tons of rare earth materials to Japan, commercially available customs data showed. That is one-third of the 2,900 tons mined by IREL, although Japan relies mainly on China for its rare earths supply.”

The Committee on Identification of Critical Minerals, Ministry of Mines recommended that CECM could be set along the lines of CSIRO.

Baskaran recommends the creation of an “anchor market” and actions to counter China could include: harmonising tariffs across anchor market countries, implementing gradually increasing quotas that require mineral inputs to be sourced from anchor market countries, and strengthening investment screening mechanisms, and when necessary, prohibiting Chinese acquisitions of critical mineral assets within anchor market countries.